I Know First Evaluation Report for Highest Implied Volatility Options

Executive Summary

In this stock market forecast evaluation report, we will examine the performance of the forecasts generated by the I Know First AI Algorithm for Highest Implied Volatility Options for long and short positions which were sent daily to our customers. Our analysis covers the period from May 15th, 2020, to October 7th, 2020.

Top Implied Volatility Options Highlights

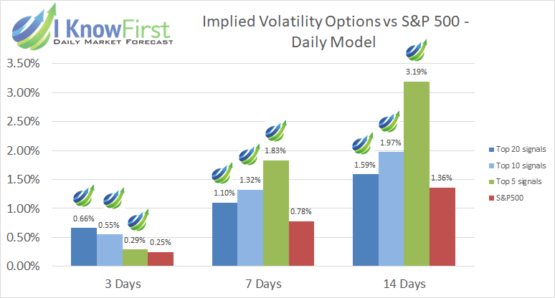

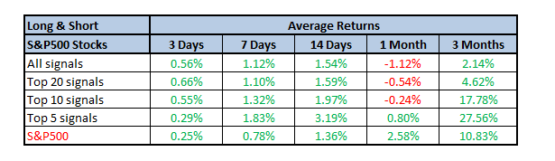

- All the signal groups’ returns on the short-term horizon outperformed the S&P 500 Index, especially the ones for the 7 and 14 days time horizons.

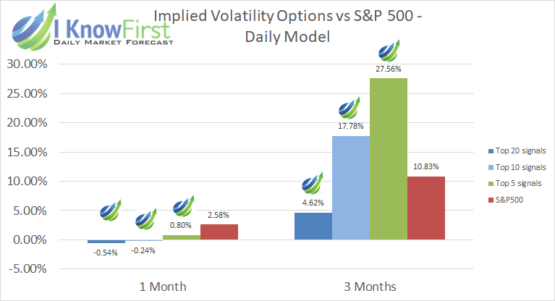

- The Top 10 and Top 5 signal groups outperformed the S&P 500 Index by over 5% and 15%, respectively, for the 3 months time horizon.

- Higher signals had higher returns for every time horizons except for the 3 days time horizon.

About the I Know First Algorithm

The I Know First self-learning algorithm analyzes, models, and predicts the stock market. The algorithm is based on Artificial Intelligence (AI) and Machine Learning (ML) and incorporates elements of Artificial Neural Networks.

The system outputs the predicted trend as a number, positive or negative, along with a wave chart that predicts how the waves will overlap the trend. This helps the trader to decide which direction to trade, at what point to enter the trade, and when to exit. Since the model is 100% empirical, the results are based only on factual data, thereby avoiding any biases or emotions that may accompany human derived assumptions.

The human factor is only involved in building the mathematical framework and providing the initial set of inputs and outputs to the system. The algorithm produces a forecast with a signal and a predictability indicator. The signal is the number in the middle of the box. The predictability is the number at the bottom of the box. This format is consistent across all predictions.

Our algorithm provides two independent indicators for each asset – Signal and Predictability.

The Signal is the predicted strength and direction of the movement of the asset. Measured from -inf to +inf.

The predictability indicates our confidence in that result. It is a Pearson correlation coefficient between past algorithmic performance and actual market movement. Measured from -1 to 1.

You can find a detailed description of our heatmap here.

Evaluating Stock Forecasts: Implied Volatility Options Package

We choose stocks from the Implied Volatility Options by taking the top 30 most predictable assets, and then we apply a set of signal-based filters: top 20, 10, and 5 based on signals. By doing so we focus on the most predictable assets on the one hand, while capturing the ones with the highest signal on the other. These forecasts are provided to our clients, which include short-term and long-term time horizons, spanning from 3 days to 3 months, and is designed for investors and analysts who need implied volatility predictions for options trading.

For the analysis, we group the forecasts by absolute signals since these strategies are long and short. If the signal is positive, then we buy, and if negative, we short.

The Stock Market Forecast Performance Evaluation Method

We perform evaluations on the individual forecast level. It means that we calculate what would be the return of each forecast we have issued for each horizon. Then, we take the average of those results by forecast horizon.

For example, we calculate the return of each trade by using this formula:

This simulates a client purchasing the asset based on our prediction and selling it exactly 1 month in the future.

We iterate this calculation for all trading days in the analyzed period and average the results.

Note that this evaluation does not take a set portfolio and follow it. This is a different evaluation method.

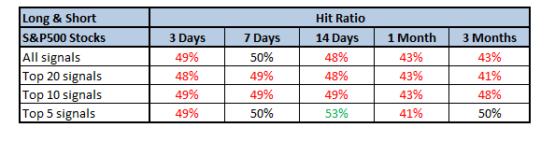

The Hit Ratio Method

The hit ratio helps us to identify the accuracy of our algorithm’s predictions.

Using our asset filtering, we predict the direction of the movement of different assets. Our predictions are then compared against actual movements of these assets within the same time horizon.

The hit ratio is then calculated as follows:

A 90% hit ratio for predictability implies that the algorithm correctly predicted the movements of 9 out of 10 assets.

The Benchmarking Method: S&P 500

In order to evaluate our algorithm’s performance, we used the S&P 500 index as a benchmark.

The S&P 500 measures the stock performance of 500 of the U.S’ largest publicly traded companies. It is one of the most followed equity indices and is frequently used as the best gauge of large cap US equities. The S&P is often used as a benchmark for the performance of US publicly traded companies, and the US market as a whole. The S&P 500 is a capitalization-weighted index, the weight of each company in the index is determined based on its market cap divided by the aggregate market cap of all the S&P 500 companies.

For each time horizon, we compare the S&P 500 performance with the performance of our forecasts.

Performance Evaluation: Overview

In this report, we conduct testing for the Implied Volatility Options Package that I Know First covers by its algorithmic forecast. The period for evaluation and testing is from May 15, 2020, until October 7, 2020. During this period, we were providing our clients with daily forecasts for stocks with highest implied volatility.

Implied Volatility Options

Every Top 10 and Top 5 signal groups outperformed the benchmark for the short term time horizons during the evaluation period. For the 7 and 14 days time periods the Top 5 signal group beat the S&P 500 index by more than 2 times. For the 3 months time horizons, the top 5 and top 10 signal groups had substantially greater performance than the benchmark index. The top 5 and top 10 signal groups had 17.78% and 27.56% for the 3 months forecasts, in comparison to the S&P 500’s return of 10.83%.

Even though the hit ratios are lower than 50% the algorithm picked the stocks with a high potential return, getting a high average returns.

Conclusion

This evaluation report presented the performance of I Know First’s algorithm for Highest Implied Volatility Options from May 15th, 2020 until October 7th, 2020. It shows the average returns and hit ratios for all time horizons.

The I Know First algorithm performed well for both short term and long term time horizons. It succeeded in generating signals which helped identifying the best opportunities during different time horizons. The higher the signals, the returns increased. The top 5 signals groups were the best performers of every time horizon except for the 3 days time period. Even in the 1-month time horizon, the top 5 signal group achieved to have positive returns.

We look forward to new market data in the following months and will monitor the changes in performance trends that are going to be communicated to our investors and subscribers in the follow-up reports.