Portfolio Strategies & Asset Allocation – 86.43% Expected Annual Return Using Algorithmic Allocation

Summary

- How to use an existing algorithmic signals system to allocate equity systematically.

- Building a sample portfolio based on stocks, interest rates, and currencies.

- Actual portfolio backtest and returns.

Introduction:

Portfolio Strategies: Allocating your portfolio in a way that maximizes returns and minimizes risk can be tricky. In order to reduce volatility, high yield strategies are often ignored. In theory, if you were able to pick one stock a day you were most certain will go up – in order to maximize expected returns you would only invest in that stock. The downside, of course, is also maximizing your risk exposure. In this article, I will go through a method of allocating funds using the I Know First artificial intelligence system. This will link between algorithmic signals, and actual market buy/sell decisions. Before you continue reading you should decide if any of these points doesn’t suit you well.

- This allocation concept is 100% systematic and is based on an existing algorithmic signals system.

- If you know how to program, you could easily turn this article into a trading algorithm that generates income, allocating by hand will require some patience and time.

- This allocation is volatile, it day trades 12 assets. Never more, sometimes less.

- This is no promotional article, I am using the I Know First system because it is the signals I have access to back test; however, you could theoretically use any similar signals generating algorithmic system (or technical analysis system).

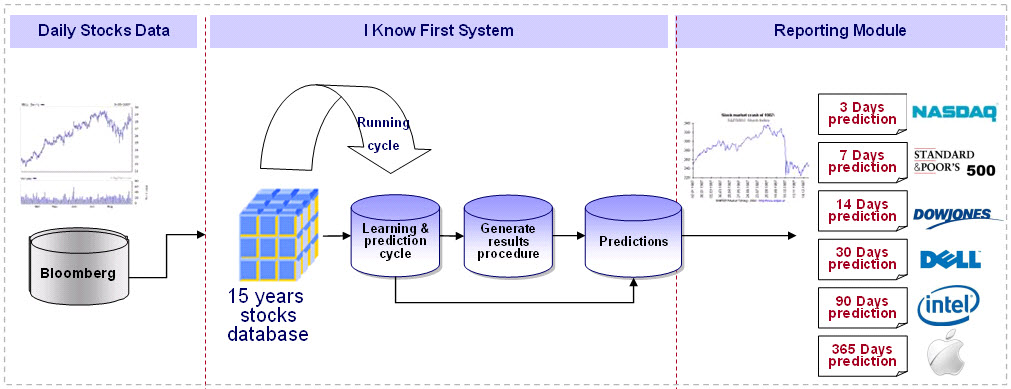

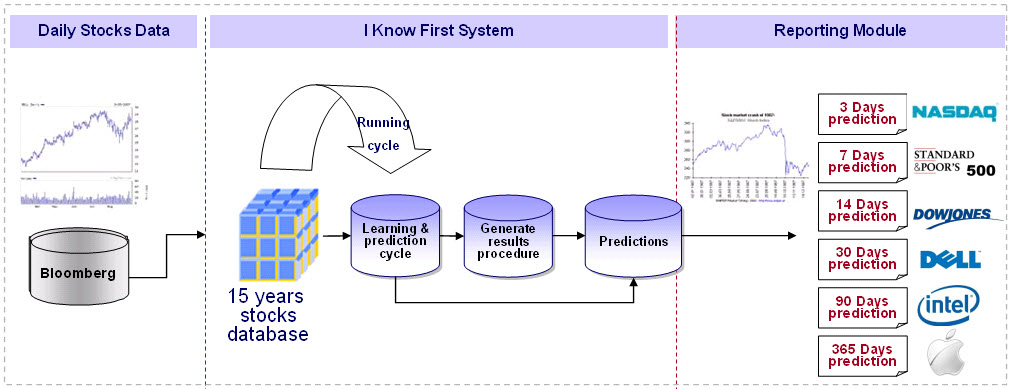

The data source

I Know First self-learning algorithm analyzes, model and predicts the stock market. The system is a predictive stock forecast algorithm that is based on Artificial Intelligence (AI), Machine Learning (ML), and incorporating elements of Artificial Neural Networks and Genetic Algorithms.

Figure 1: Example of the algorithmic system used to generate the data.

I Know First Market Prediction System models and predicts the flow of money between the markets. It separates the predictable part from stochastic (random) noise. It then creates a model that projects the future trajectory of the given market in the multidimensional space of other markets.

The system outputs the predicted trend as a number, positive or negative, along with the wave chart that predicts how the waves will overlap the trend. This helps the trader to decide which direction to trade, at what point to enter the trade, and when to exit.

The model is 100% empirical, meaning it is based on historical data and not on any human-derived assumptions. The human factor is only involved in building the mathematical framework and initially presenting to the system the “starting set” of inputs and outputs.

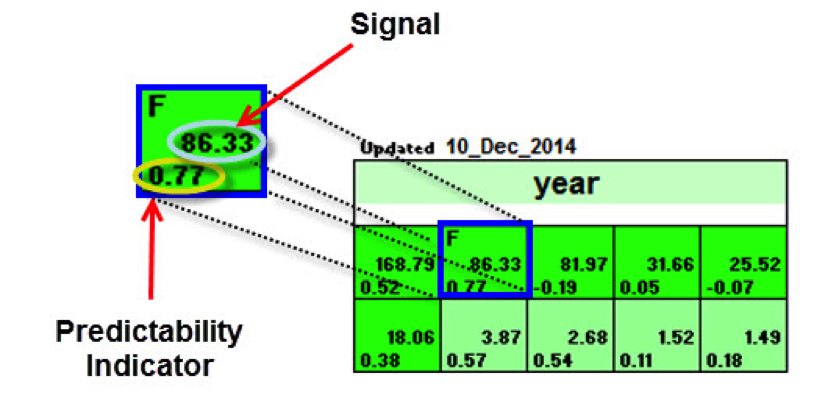

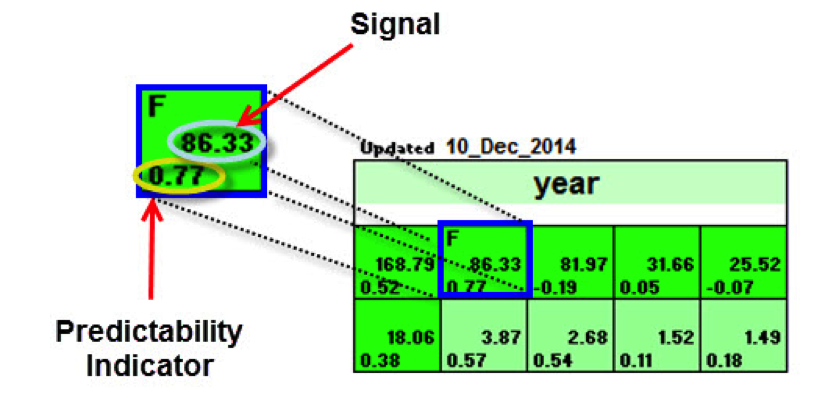

The algorithm produces a forecast with a signal and a predictability indicator. The signal is the number in the middle of the box. The predictability is the number at the bottom of the box. At the top, a specific asset is identified. This format is consistent across all predictions.

Figure 2: A sample of an algorithmic table demonstrating the position of the signal and predictability indicators.

The signal represents the predicted movement direction or trend and is not a percentage or specific target price. The signal strength indicates how much the current price deviates from what the system considers an equilibrium or “fair” price. The signal can have a positive (predicted increase) or negative (predicted decline) sign. The heat map is arranged according to the signal strength with strongest up signals at the top while down signals are at the bottom. The table colors are indicative of the signal. Green corresponds to the positive signal and red indicates a negative signal. A deeper color means a stronger signal and a lighter color equals a weaker signal.

The predictability indicator measures the importance of the signal. The predictability is the historical correlation between the prediction and the actual market movement for that particular asset, which is recalculated daily. Theoretically, the predictability ranges from minus one to plus one. The higher this number is the more predictable the particular asset is. If you compare predictability for different time ranges, you’ll find that the longer time ranges have higher predictability. This means that longer-range signals are more important and tend to be more accurate.

Building the Allocation

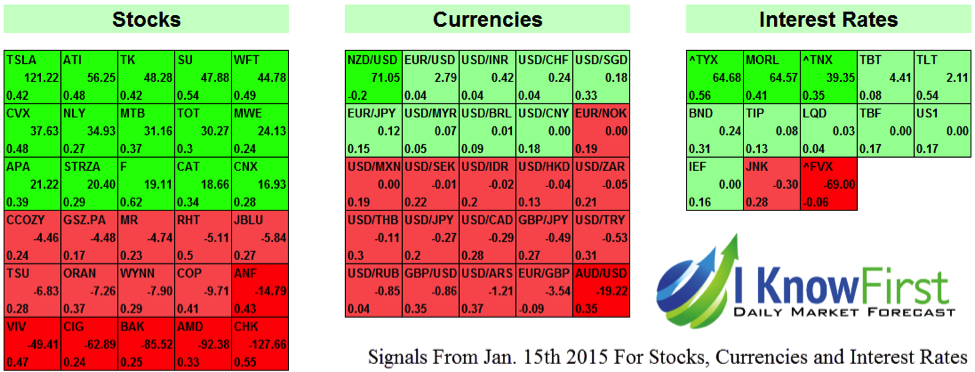

I Know First tracks stocks, commodities, currencies, indexes, ETF’s, and many other assets. For this allocation model we will focus on stocks, interest rates, and currencies; however, you could use any signals for any type of asset in a similar manner. Below is the example of the three 1 month forecasts from January 15th, 2015 used in order to trade that day.

Figure 3: Actual forecasts from Jan 15th, 2014 before the market opening. Example: Strongest bullish stock is TSLA (signal 121.22), and the strongest bearish stock is CHK (signal -127.66).

We are looking for the 4 strongest signals (middle number), in terms of absolute value, for which the following rule holds true before the market opens.

- The current price is above the 5 days moving average (long position) for a positive value signal (marked in green).

- The current price is below the 5 days moving average (short position) for a negative value signal (marked in red).

We then convert all signals to their absolute value and use them as our variable allocation base. For example, if the four top signals are (10, 20, 30, and 40) the variable allocation would be (10%, 20%, 30%, and 40%). The natural allocation would always be 25% (Because we trade 4 assets a day). The customized allocation is then the combined weight of both, set according to pre-determined rule. We would then repeat this process daily always adjusting the allocation between assets. Bellow you can see the trades detected in each separate asset class according to the system on that particular date. The base is simply cash and is used when not enough trades matching the rules are detected that day. Rather than investing funds in non-optimal opportunities we hold the cash for a better outlook.

Trade Results

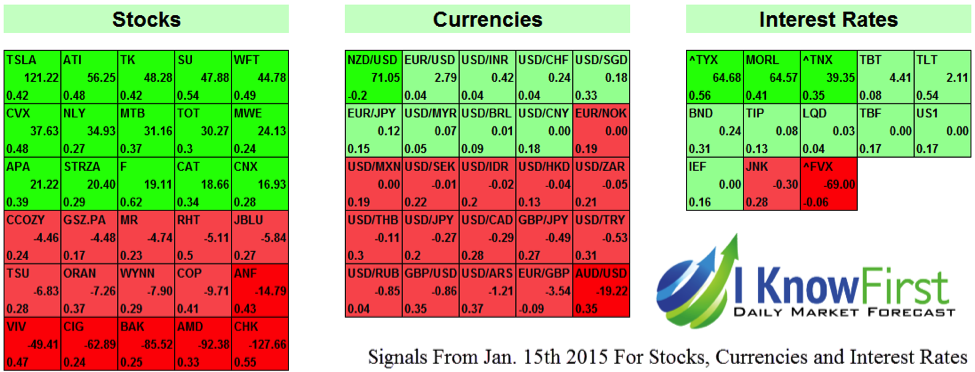

Figure 4: The allocation for stocks, as you can see TSLA didn’t make the cut as its previous close was below the moving average of the price. Similarly, CHK was not added either as its previous close was above the moving average.

Figure 5: The signal filter of 1 (all lower signals are ignored) means there are only 5 opportunities – of which only two match the moving average rule, thus we short ^FVX and long TLT.

Figure 6: Only one currency made the cut EUR/GBP. Please note that currencies are leveraged to a multiple of 10 meaning the actual percent change was -3.60% and the change in equity was $155.

We would then divide the portfolio between the three main asset classes. As part of the analysis for a client, we backtested this strategy for 7 months, below are my results using an allocation of 60% stocks, 30% interest rates, and 10% currencies with a leverage of 10. In order to understand better how the allocation is done the image below shows an example of 50% variable allocation weight for all three asset classes

Figure 7: Visual representation of the allocation process.

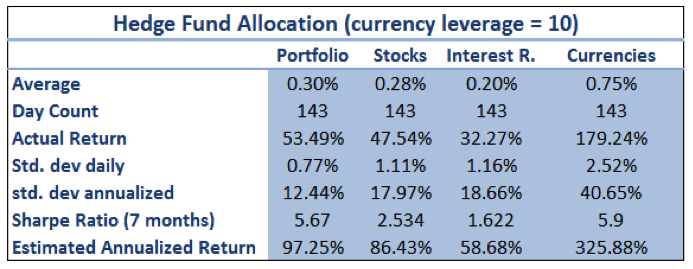

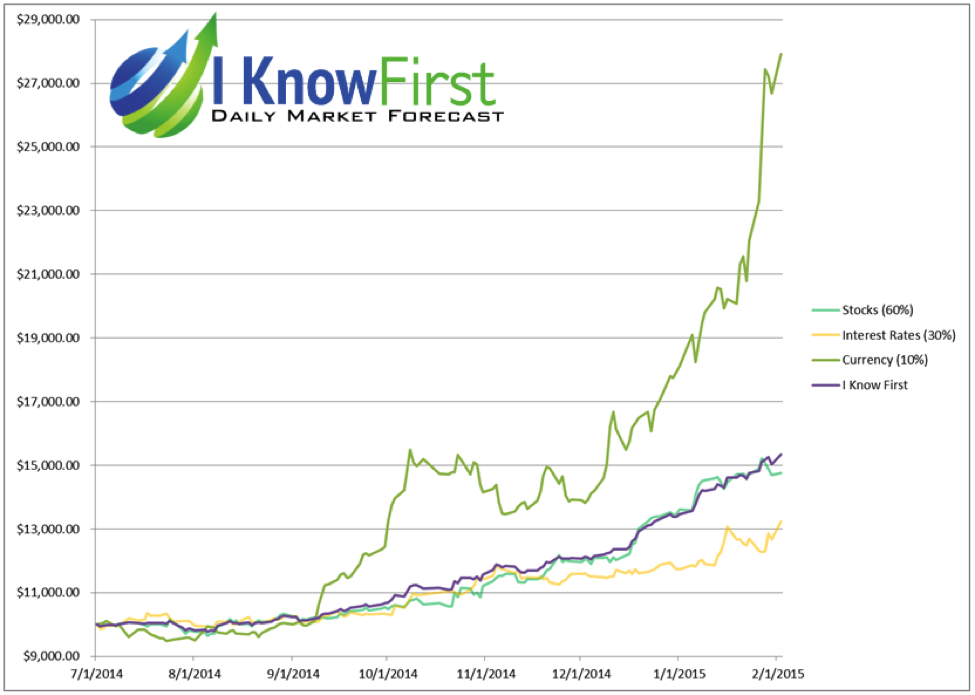

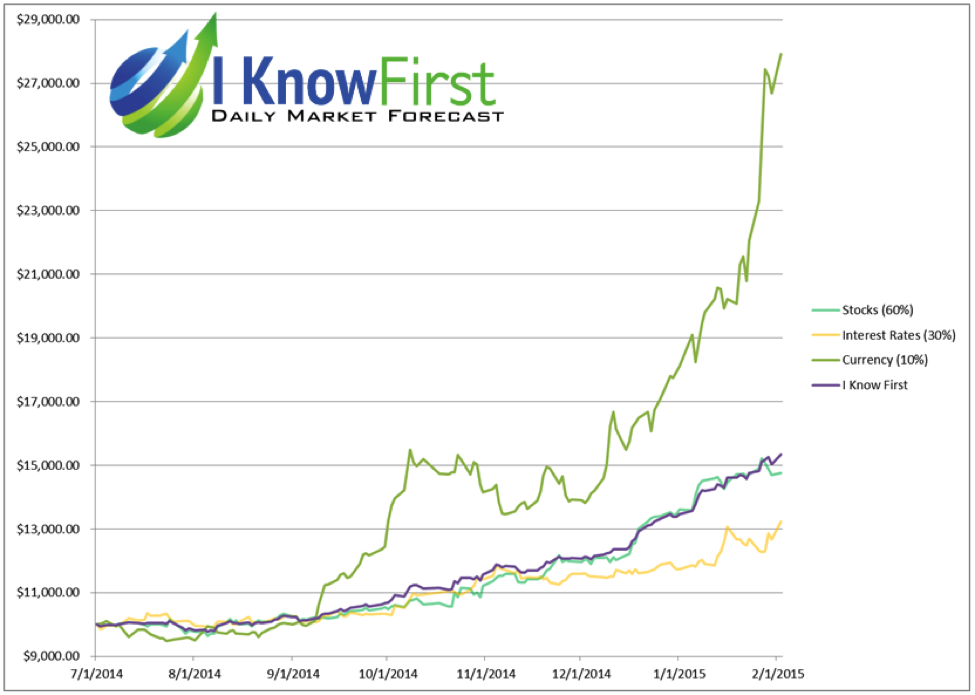

The backtest was made from the 1st of July 2014 to the 1st of February 2015, a 7 months period. The results for the portfolio and each separate class look as follows.

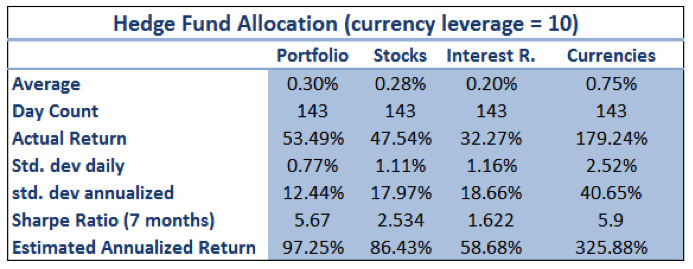

Figure 8: 7 months backtest results of separate classes and combined portfolio.

Figure 9: 7 months line graph of backtest results of separate classes and combined portfolio.

The highest daily return was for the I Know First portfolio (not counting leverage on currencies). The average daily return was 0.30% with a standard deviation of 0.77%. While the risk might seem very high (and it is for most hedge funds), a turbo fund could boast the high Sharpe ratio, which measures the risk to reward ratio of a portfolio. Generally, a ratio above 2.5 is considered good.

End Note

The main advantage of this portfolio allocation is that it is a day trading model which is 100% systematic. Both the investment buy/sell decisions and allocation are based off the signal data; allowing any investor the peace of mind in separating emotion from trade decisions. Finally, with the advancement and cost effectiveness of technology improving rapidly in recent years, data which was once available only to banks and large institutions, is now also available to private investors – significantly evening out the playing field. Proper allocation and money management and the emotional influence of private investors are one of the main reasons most private traders are still unprofitable. This model looks to solve those two problems.

I Know First Research is the analytic branch of I Know First, a financial startup company that specializes in quantitatively predicting the stock market. This article was written by Daniel Hai. We have no business relationship with any company whose stock is mentioned in this article.