Stock Market Prediction: Investment in the Best Industries (GICS Level 2)

Stock Market Prediction: I Know First provides investment solutions for both individual and institutional investors, utilizing an advanced AI self-learning algorithm to gain a competitive advantage. We offer a personalized approach to our institutional clients, assisting them in their investment process based on their specific needs and preferences. For more details about I Know First solutions for institutional investors, please visit our website.

Stock Market Prediction: Investment in the Best Industries (GICS Level 2)

Stock Market Prediction: The following trading strategy was developed using I Know First’s AI Algorithm daily forecasts from January 1st, 2020, to December 31th, 2023, with a focus on S&P 500 stocks selected based on the signal filter. This strategy is available to our institutional clients: hedge funds, banks, and investment houses, as a tier 2 service on top of tier 1 (the daily forecast).

The strategy involves trading GICS level 2 ETFs based on the majority direction. While, the Level 1 Sectors include broad segments of the economy, such as technology, healthcare, finance, and consumer goods to provide a high-level view of the market. Level 2 Industries goes deep into specific industries. For example, within the technology sector (Level 1), you might find industries like semiconductors, software, and hardware. These industries offer a more detailed perspective on the market.

The term “majority direction” refers to our predictions for stocks, upon which we base our position. This decision is guided by a number of long and short stock forecasts. Therefore, if the count of long stock forecasts surpasses the count of short stock forecasts, the majority direction is to go long and we construct a long portfolio. Conversely, if the count of short stock forecasts is higher, we assume a short portfolio.

We select the 3 industries with more stocks from a selected stock universe based on the signal filter. ETFs in our portfolio are weighted depending on how many stocks from the selected stock universe in each industry. For example, if 10 stocks are from XHB, 5 from XTL, and 5 from XRT, it would be weighted as 50%, 25% and 25% in the portfolio.

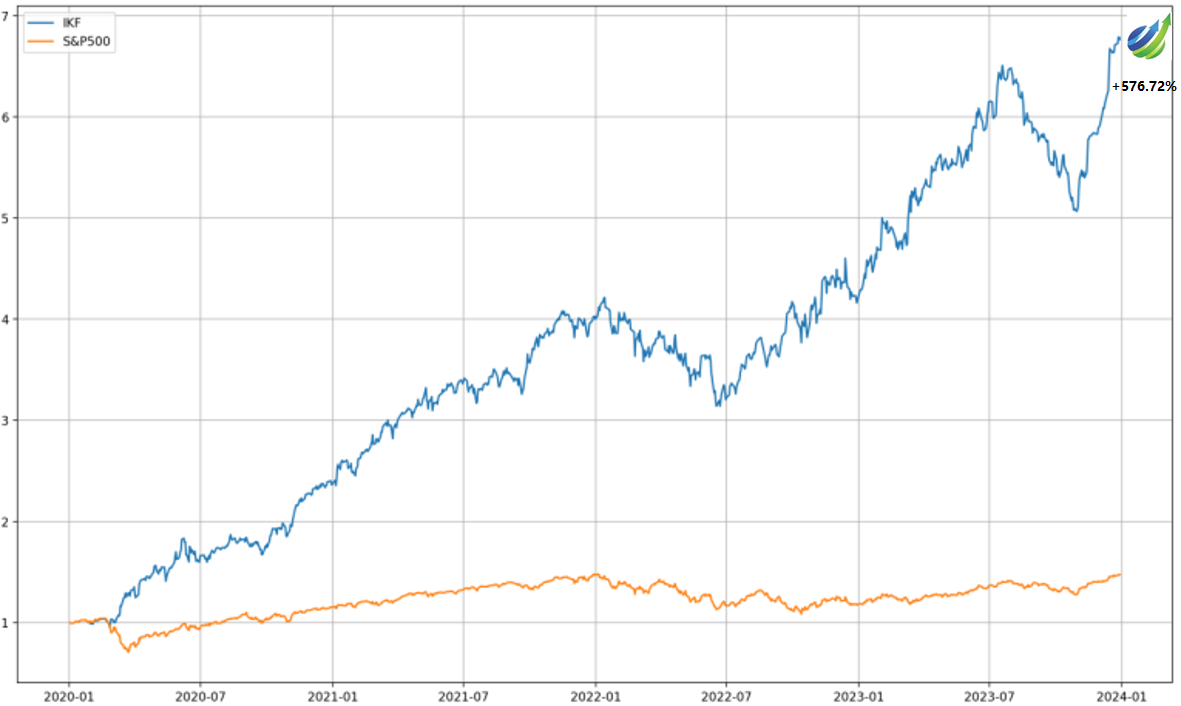

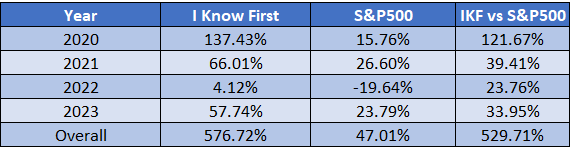

The strategy provides a positive return of 576.72% which exceeded the S&P 500 return by 529.71%. Below we can notice the strategy behavior for each year. Below we can notice the strategy behavior for each year.

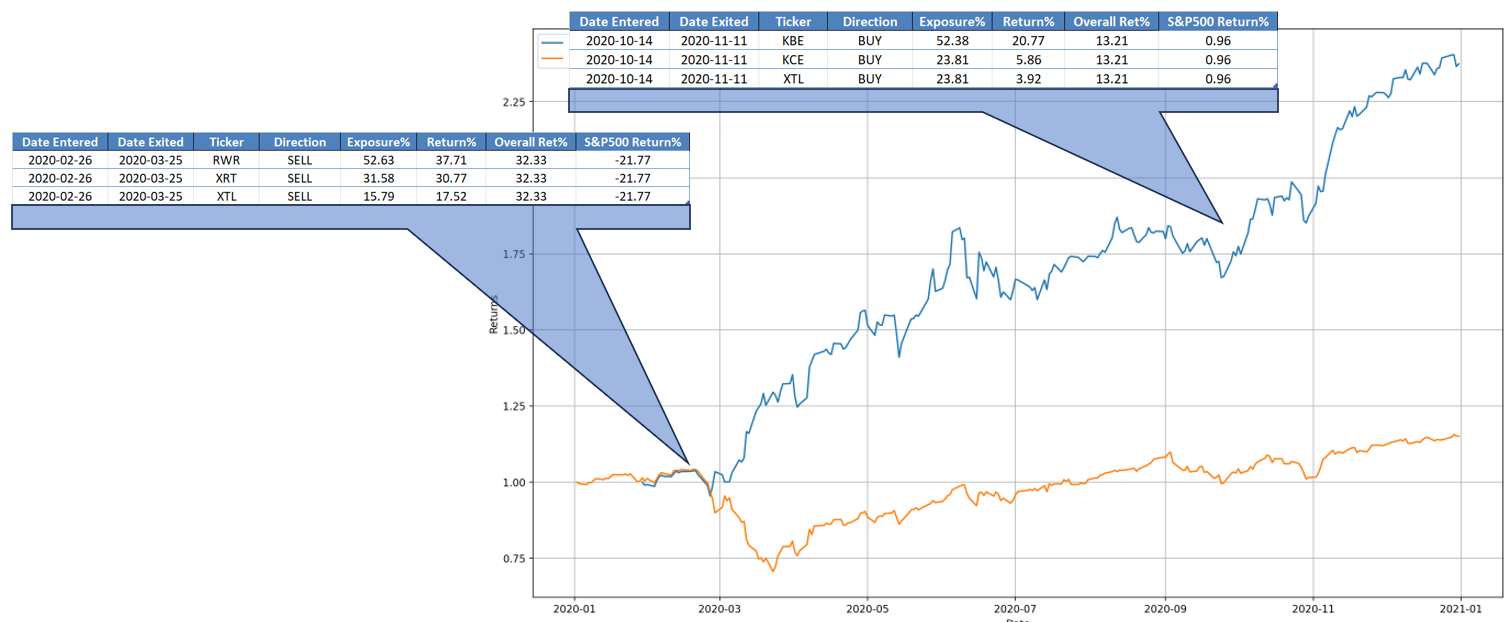

The strategy provided a positive return of 137.43%, exceeding the S&P 500 return by 121.67% in 2020. We can observe impressive periods during which the strategy significantly outperformed the S&P 500. From February 26th to March 25th, the strategy selected short positions in RWR, XRT, and XTL with weights of 52.63%, 31.58%, and 15.79% respectively, yielding a return of 32.33% and enabling it to outperform the S&P 500 by 54.1%. From October 14th to November 11th, the strategy selected long positions in KBE, KCE, and XTL with weights of 52.38%, 23.81%, and 23.81% respectively, resulting in a return of 13.21% and enabling it to outperform the S&P 500 by 12.25%.

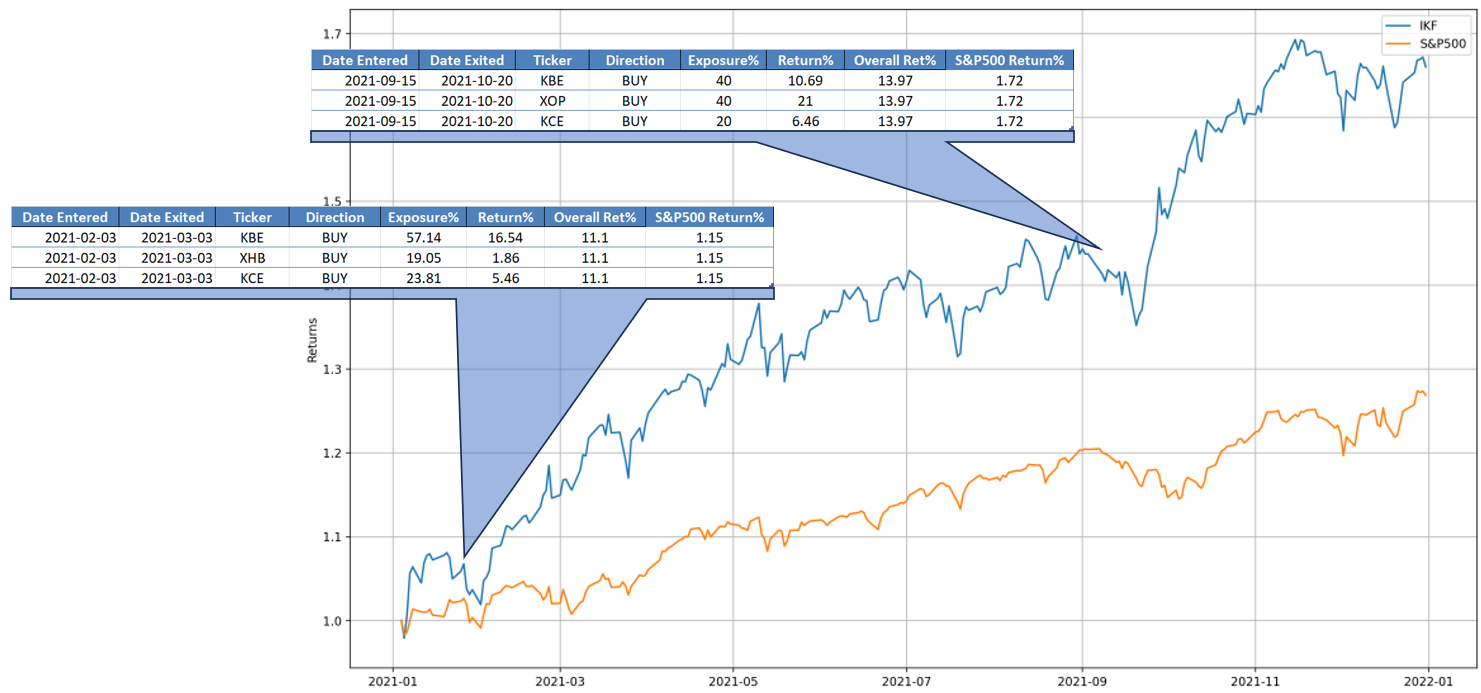

The strategy provided a positive return of 66.01%, exceeding the S&P 500 return by 39.41% in 2021. We can observe impressive periods during which the strategy significantly outperformed the S&P 500. From February 3rd to March 3rd, the strategy selected long positions in KBE, XHB, and KCE with weights of 57.14%, 19.05%, and 23.81% respectively, resulting in a return of 11.1% and enabling it to beat the S&P 500 by 9.95%. From September 15th to October 20th, the strategy selected long positions in KBE, XOP, and KCE with weights of 40%, 40%, and 20% respectively, resulting in a return of 13.97% and enabling it to beat the S&P 500 by 12.25%.

The strategy provided a positive return of 4.12%, exceeding the S&P 500 return by 23.76% in 2022. We can observe impressive periods during which the strategy significantly outperformed the S&P 500. From August 24th to September 21st, the strategy selected short positions in KIE, RWR, and XTL with weights of 20%, 46.67%, and 33.33% respectively, resulting in a return of 7.24% and enabling it to beat the S&P 500 by 13.85%. From September 21st to October 5th, the strategy selected short positions in RWR, XRT, and XTL with weights of 52.94%, 23.53%, and 23.53% respectively, resulting in a return of 4.03% and enabling it to beat the S&P 500 by 7.56%.

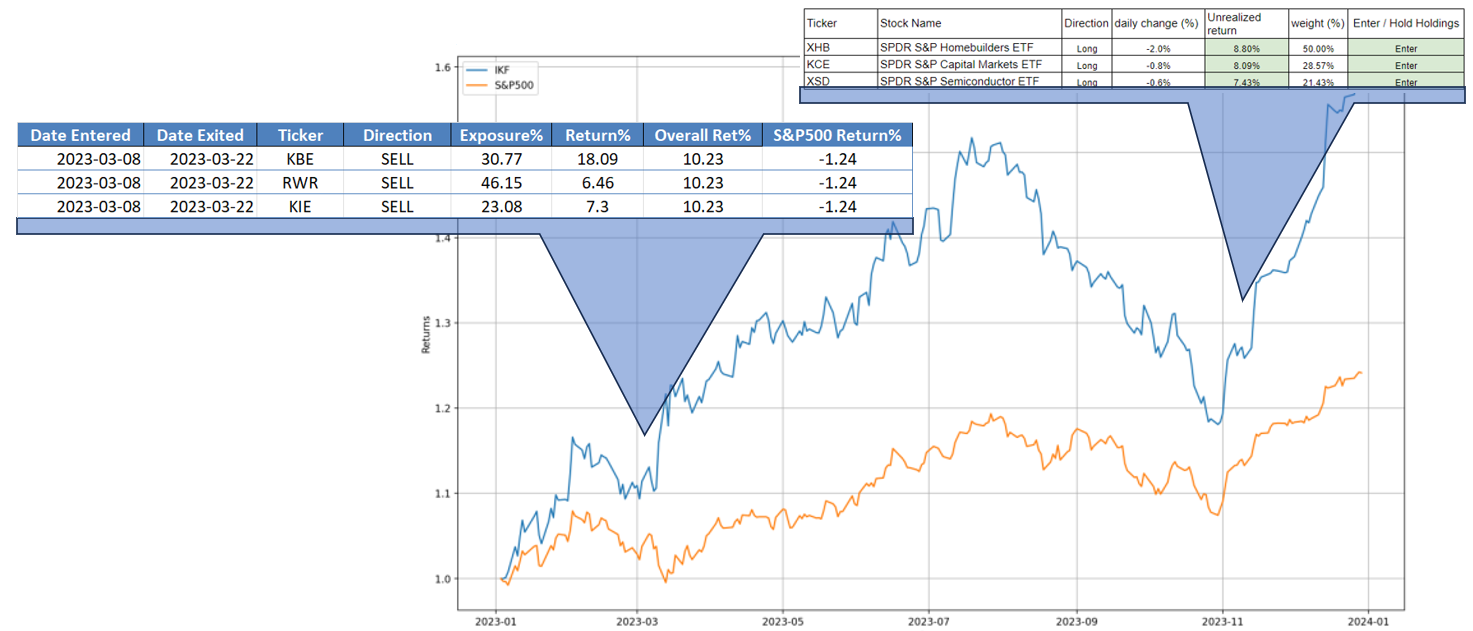

The strategy provided a positive return of 57.74%, exceeding the S&P 500 return by 33.95% in 2023. From March 8th to March 22nd, the strategy selected short positions in KBE, RWR, and KIE with weights of 30.77%, 46.15%, and 23.08% respectively, resulting in a return of 10.23% and enabling it to beat the S&P 500 by 11.47%.

I Know First Algorithm – Seeking the Key & Generating Stock Market Forecast

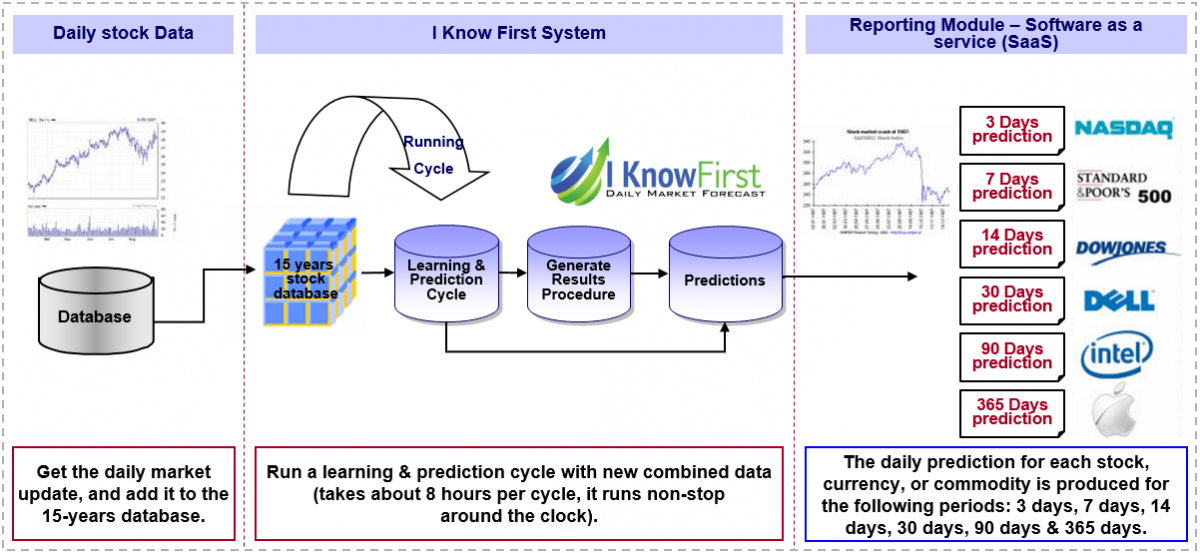

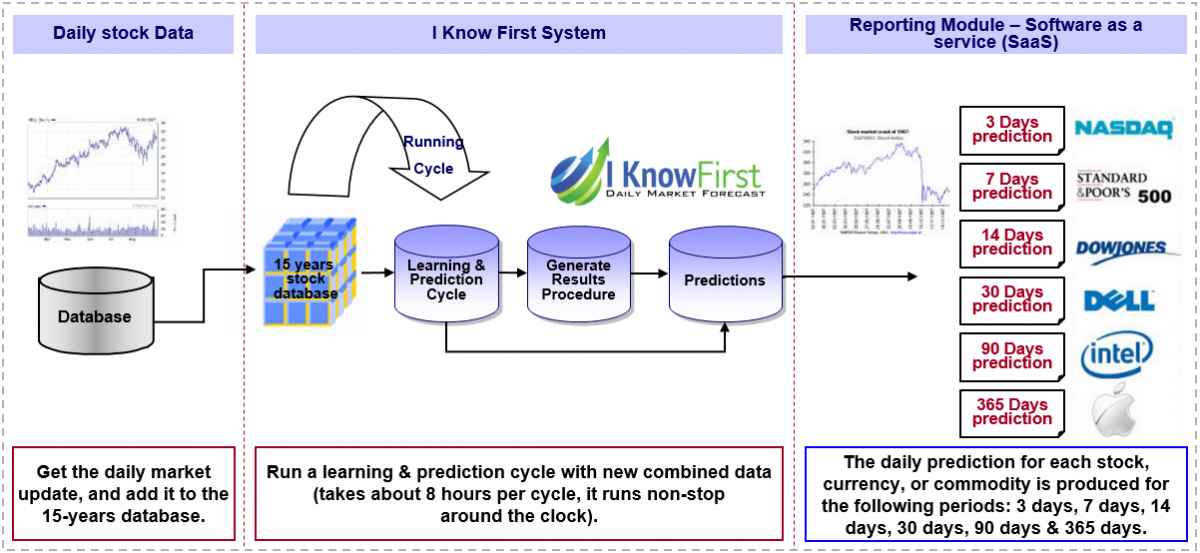

Stock Market Prediction: The I Know First predictive algorithm is a successful attempt to discover the rules of the market that enable us to make accurate stock market forecasts. Taking advantage of artificial intelligence and machine learning and using insights of chaos theory and self-similarity (the fractals), the algorithmic system is able to predict the behavior of over 13,500 markets. The key principle of the algorithm lies in the fact that a stock’s price is a function of many factors interacting non-linearly. Therefore, it is advantageous to use elements of artificial neural networks and genetic algorithms. How does it work? At first, an analysis of inputs is performed, ranking them according to their significance in predicting the target stock price. Then multiple models are created and tested utilizing 15 years of historical data. Only the best-performing models are kept while the rest are rejected. Models are refined every day, as new data becomes available. As the algorithm is purely empirical and self-learning, there is no human bias in the models and the market forecast system adapts to the new reality every day while still following general historical rules.

Conclusion

I Know First offers investment solutions for institutional investors, leveraging our advanced self-learning algorithm to gain a competitive advantage. We provide a personalized approach for our institutional clients, enhancing their investment process according to their specific needs and preferences. In this context, we have evaluated the performance of the investment in the best industries strategy contents Industries in GICS Level 2 during the period from January 1st, 2020, to December 31st, 2023.

To subscribe today click here.

Please note-for trading decisions use the most recent forecast.